|

10/24/2018 0 Comments Investing in the Overseas MarketIt has been a challenging year for investing in foreign markets. Economic growth has diverged between the U.S. and non-U.S. regions and equity markets have followed suit. It has been a challenging year for investing in foreign markets. Economic growth has diverged between the U.S. and non-U.S. regions and equity markets have followed suit. However, the conditions that led to weakness in international markets and strength in the U.S. could well reverse in the latter part of this year. In the U.S., the Federal Reserve is likely to keep raising interest rates, earnings growth is at a peak and market leadership in the tech and consumer discretionary sectors is looking vulnerable. In contrast, beyond U.S. shores, monetary policy remains loose, growth could be stabilizing, and valuations appear more attractive.

Recent weakness in certain foreign markets can provide an opportunity to rebalance your portfolio and avoid being overexposed to late-cycle U.S. markets. Below are three regions that could represent opportunities going forward: Europe – Stocks may have sold off more than financial conditions warrant, creating some compelling opportunities. Investors should look for high-quality, value-oriented Europe sectors with less U.S. exposure, such as financials, utilities and telecom. Japan – Its labor market is seeing the most improvement in decades and business sentiment is up. Corporate profitability and earnings momentum are improving. These conditions may support growth and benefit equities. Emerging Markets – The downturn in currencies and stocks may be overdone. China weakness seems overstated and a rebound once currency and headline fears abate may benefit emerging markets. Investors should stay with export-oriented emerging market countries that are less sensitive to dollar strengthening, such as Russia, Taiwan and Korea.

0 Comments

Investors saw very positive results in private markets for FY 2017; the year marked a record year for fundraising in private markets, with over $750 billion globally raised. PE and private debt grew by 11 percent and 10 percent respectively. Most growth derived from funds with AUM of over $5 billion. Notably, ignoring megafunds, the market activity from all other funds decreased. As numbers are finalizing for the year of 2018, investors see funds raised thus far down about 40%, while aggregate capital raised within PE is down about 30%. Overall operating metrics for the industry appear healthy, with dry powder to deal volume at a healthy ratio and stable over time. Interestingly enough, pension funds are increasingly allocating to the asset class year over year, as well as sovereign wealth funds who are becoming more and more important. Investors should see co-investment deals increasing over the next few years.

On overall economic news and activity, it appears as if greater degree of discipline is taking place than during the run up to historic financial crises. Rather than underwriting at any cost and blowing up deal multiples, most of the PE managers are hedging towards multiples contraction. Keith Knutsson of Integrale Advisors commented, “Even if results for FY 2018 might not appear as strong as the previous year, I think the Private Equity market is strong going forward. One thing investors should keep an eye out for is whether the decrease in deal activity continues, and dry powder increases at similar rate.” The argument whether enhanced regulatory oversight by the Consumer Financial Protection Bureau (CFPB) has a significant impact on the supply of credit or on bank-risk taking is a critical topic. With regulatory efforts strengthening across the street, one might assume that the non-agency lending business has been negatively impacted. However, studies from reports showcase that CFPB oversight has at most a small negative effect on overall mortgage lending. According to the research done, an increase in regulatory effort creates an environment where banks decrease origination for riskier loans. That might be the case for riskier loans, but non-qualified mortgage loans are not necessarily considered risky.

The non-qualified mortgage loans of today are nothing like the subprime loans of yesterday. Even with non-QM loans, a lender must follow all requirements and validate the borrower’s “ability-to-repay”. This would mean vetting all the applicants with employment, income and asset verification similar to that of agency loans. Non-QM loans are not as risky because lenders offset some of the risk by charging higher rates and fees as long as they can demonstrate the consumer’s “ability-to-repay” debt. Jumbo mortgages are also affected by an increase in regulatory burden because they fall outside of the QM rule standards and thus don’t fall under the safe harbor, making lenders reluctant to originate them. After examining the regressions, applicant denials and graphical evidence from reports, it is clearly evident that the CFPB oversight has affected the composition and riskiness of bank lending. Keith Knutsson suggests "The 'pendulum' had swayed too far to the radical side of regulation. This has left a gap in the market where worthy loans have been widely ignored by the institutions. Thus proving that heavy regulations have been more of a burden, than a benefit, in the non-QM lending business. This neglect in the industry has created an opportunity for institutions to capitalize on what would normally be healthy loans." Events that have recently been triggering the market have stimulated investor curiosity around the relationship between government bonds and the returns of equities. Looking back, the S&P 500 took a major downturn in January and February of 2018 due to poor market conditions. Not only that, but the 10-year government bonds also showed a positive trend from 2.6% - 2.8% in the beginning of the year. The reputation of bonds as a “safe-haven” asset during a time of crisis is being questioned by investors all around the world today.

With the recent rise in bond yields due to positive results in hourly earnings numbers and payroll, investors reassessed their outlook on inflation. This was backed by a slight increase in bond yields. Simply put, investors believe the shock started spreading from the equity market from the gecko. This is truly inaccurate and a major misconception as the shock emanated primarily from the bond market instead of the equity market. In theory, the relationship between bonds and stocks largely depend on whether a shock starts in the bond market or stock market. It is important to note that bond market shocks induce a positive stock-bond relationship, whereas equity market shocks prove a negative relationship due to the association with the flight-to-quality (FTQ). Government bonds have shown strong performance in nearly all types of economic recessions regardless of investors deciding to be proponents of this theory or not. These bonds have not only shown growth in the last six decades but have also served to act as a way to hedge against pro-cyclical equity exposure. We use equity prices to better understand the value of a set of discounted future cash flows. There is a major impact on the discount rates due to a shock in the real bond market. This lowers the stock price and increases equity yield thus capturing higher real rates. However, whenever FTQ occurs aka a negative shock in the equity market, bond yields fall as the bond market seems much more favorable to investors. Looking at equity risk premium, FTQ occurrences seem to be related to a slightly noticeable negative stock-bond relation, while real yield shocks result in a positive market correlation. When markets are expensive, equities become vulnerable to negative bond market shocks and rises in bond yields. Moving forward, this rise in bond yields will serve to be a risk that investors should be aware of and must consider when flocking to either side of the market in search for safe-haven assets. President Donald Trump has officially set out his plan to impose tariffs on steel and aluminum imports with China. Tariffs of 25% on steel imports and 10% on aluminum imports will result in a price increase for multiple consumers and slow down growth for many businesses globally. The rising tensions between China and the U.S. might seem like a time to move away from most growth-sensitive asset classes, but investors could be wrong.

The announcement resulted in a decline in the stock market as oil and metals started taking a big hit, but could this be a great opportunity to buy industrial metals? Copper has already fallen sharply by 4% in one month, while other oil and metal commodities follow the decline. Investors shouldn’t be too pessimistic and consider the chance of current tensions not escalating into a full-blown trade war. This is thanks to China’s massive stimulus during the financial crisis which is set to offer another boost to global metals prices. Commodity analysts predict, “The resulting acceleration in metals demand is expected to push the copper market, as well as other base metal markets such as nickel and zinc, into deficit, leading to inventory draws, a tightening of the future curve spreads, and higher prices.” We need to further investigate the backdrop to understand why a trade war might positively impact industrial metals. Looking back into December 2017, we have seen prices of aluminum and copper trend upwards even before rumors of a trade war started. Even though global trade remains strong, Chinese credit growth, a leading commodities indicator showed staggering trends in 2017. This means China’s President Xi Jinping will start another round of debt-fueled stimulus to repair the debt problem. Simply put, as long as China is tapering credit growth, the small increase in global trade won’t be an “unalloyed” positive for commodities. Alternatively, a high intensity trade war could initially hurt commodity prices but raise the probability of another round of stimulus in China in the next few years. Being wary of this stimulus will give investors an opportunity to buy during the dip and see industrial metal prices trend upwards. As of right now, Germany is falling short of its European climate targets and will have to pay for access to produce and emit greenhouse gases due to the nations polluting farms, factories, and vehicles. This comes after Chancellor Angela Merkel, a longtime proponent of reducing emissions. delivered the news. As a result, Germany will now have to purchase greenhouse gas emissions allowances for the following two years from other European Union members.

“Germany has been on the forefront of industrial production in Europe for many years. However, every nation must choose a proper balance of economic growth that will not cause substantial, irreversible damage to the environment” said Keith Knutsson of Integrale Advisors. The extent of the shortfall will only be known after these next couple of years. The permits will then be purchased from another country in the European Union. This price can vary and has yet to be determined. One thing we do know, is it will come at the price at the expense of German taxpayers. As part of Germany’s agreement to prevent global warming under last year’s Paris Accord, the European Union has pledged to curb global warming by continuing to pursue reductions in carbon discharges not only for industrial production but also for agriculture and waste. A previous report from the European Commission displayed that emissions from the European Union would remain below the 2020 target, with 21 member States expected to keep or reduce their emissions below their national targets by 2020. 1/18/2018 0 Comments German Economic GrowthIn 2017, Germany’s economy grew at the fastest annual pace in nearly a decade. As a result, this is a large contribution to the pickup in growth across the eurozone.

According to the German National Statistics Office, GDP (gross domestic product) grew 2.2% last year, after analysts expected growth of 2.3%. Nevertheless, it was the fastest pace of growth recorded since 2011. Germany’s strong performance feeds into the success of the eurozone. On Tuesday, the World Bank estimated the EU’s economy grew 2.4% in 2017, which would be its strongest performance since 2007. The expectation is that Germany’s positive growth and momentum will continue in the current year. Trade played a big role in the growth: imports grew 5.2%, exports were up 4.7%. “Looking to the future, the fundamental factors that supported growth in 2016 and 2017, such as rising industrial production and larger demand for real estate, should still be in place in 2018” said Keith Knutsson of Integrale Advisors. The recent pickup in growth across the eurozone has made policy makers at the European Central Bank more confident that they will reach their inflation target over the next couple of years. The central bank is decreasing monthly bond purchases under the quantitative easing program from €60 billion from €30 billion. The acceleration in growth has been fueled in part by a rise in business investment, with Germany seeing a 3.5% rise in spending on domestic plant and machinery in 2017. Eurozone industrial production was 1% higher than in October, and 3.2% higher than in November of 2016. As a result, Germany remains the Eurozone’s manufacturing powerhouse. Low inventory and interest rates in the real estate sector colluded to attract foreign investment, surging prices in the housing market of Australia in the past. According to the Bureau of Statistics, Sydney’s residential property price index has increased some 70% during the past five years, reaching a peak in 2014. The real estate industry’s outlook remains strong, even though growth rates are expected to slightly decelerate overall in the coming years due to government intervention on foreign investments.

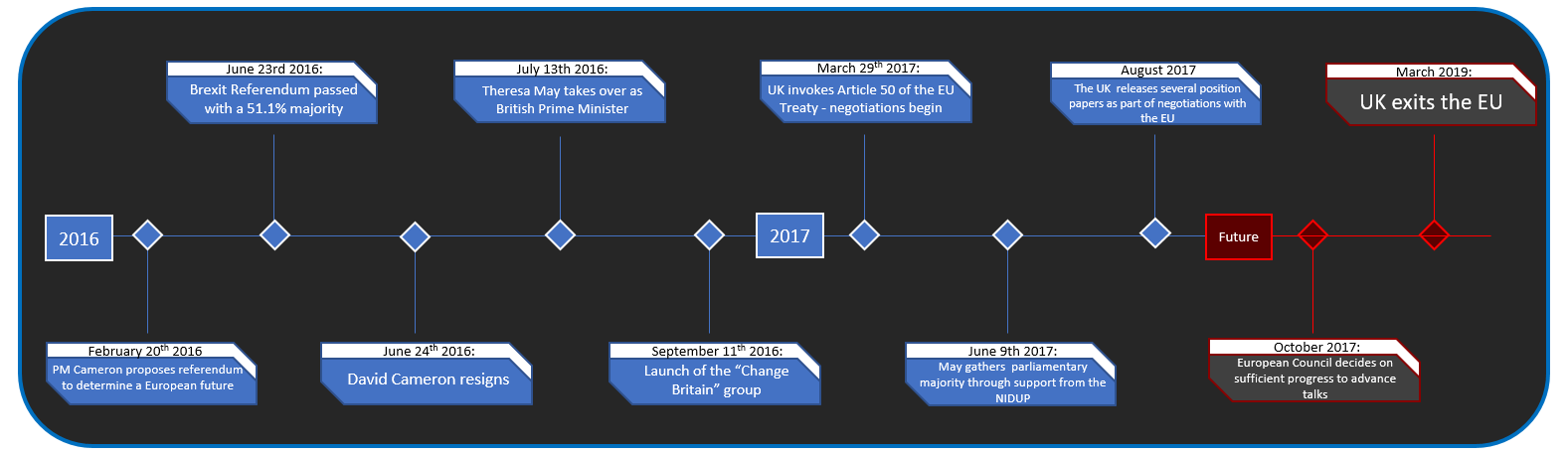

Especially China, the biggest group of foreign buyers in the Australian real estate market per the Foreign Investment Review Board, has been deterred from further investments. From 2015 to 2016, Chinese investors spent $32 billion, mostly in Sydney and Melbourne, four-times the amount US residents spent. Foreign investment in the past has been restricted to only new developments, but with recent regulations Rules for developers have changed too - now only half the dwellings in new developments can be sold to foreign investors. Additionally, the government has enacted charges of between 1.4-to-5.5 per cent — depending on the value of the property— as well as a vacant property tax of 1 per cent. Keith Knutsson of Integrale Advisors commented, “Regulation on foreign investment certainly slows down asset management services in Australia, but building and construction contractors as well as property agencies will remain, with increasing strength, to be key suppliers to this low inventory market. Australia is continuing to look for those services, no matter where the capital originates from. Yet, enormous capital requirements might limit new entrants from entering the market.” As the clock on Brexit negotiations is ticking, Britain’s political winds are shifting. In two months, the European Council decides whether Brexit negotiations can advance to focus solely on future relationship and any potential transitional deal based on a report of the Chief negotiator Michel Barnier. Currently the logistics of managing the actual political exit of Britain are slowing down proceedings. To understand future developments, it’s vital to begin with an understanding of the events leading up to Brexit. Keith Knuttson of Integrale Advisors says:” Over the past few months an array of invalidated speculation has played a part in shaping the misunderstandings regarding the proceedings in the UK. It is vital to remain conscious of ideas that were based on erroneous information.” David Cameron spoke of Brexit for the first time in February 2013: a referendum on Britain’s membership to the EU if the Conservative party is elected in the next general election. At the time, Cameron was trying to quell euro-skeptics within his own party. A year and a half later Scotland held a referendum on its own independence from the UK, but voters wanted to remain in the UK. The sentiment of Scots to remain in the UK and Europe caused further division within Brexit negotiations months later. In May 2015 Cameron’s party wins and British voters elect a majority Conservative government. During his victory speech Cameron mentions that there will be a referendum on EU membership. Cameron announces that he has negotiated a deal with EU leaders which will give Britain a “special status” if it stays in the EU. Then on February 2016 Cameron announces his official position and starts to campaign for the remain movement. A previous political ally to Cameron, Boris Johnson, proceeds to join the leave campaign on February 21st – shifting tides towards Brexit. On June 16th 2016 ardent remain campaigner Jo Cox is shot and stabbed in the street in her electoral district in northern England by the extremist Thomas Mair who shouted “Britain first, Keep Britain independent, Britain always comes first.” Both sides temporarily suspended campaigning ahead of the referendum. One week later the UK voted 51.1% in favor of Brexit with a turnout of 72.2%.  8/27/2017 0 Comments The Global EconomyThe world’s major economies are growing harmoniously, a result of persistent low-interest-rate stimulus from central banks around the world and the rise out of debt for nations faced with political and economic uncertainty, such as Greece and Brazil.

The OECD, Organization for Economic Cooperation and Development tracks the progress of its 45-member states. These nations are on track to grow this year, and 33 of them are projected to accelerate significantly from the previous year, according to the OECD. “For the first time in years we are seeing signs of continuous, synchronized economic expansion on the international front” said Keith Knutsson of Integrale Advisors. U.S. U.S. exports rose 6% in the first half of the year, the best two-quarter performance since the end of 2013. The post-election period has been categorized by economic strength as well record-breaking index growth, such as the DJA and Nasdaq averages. In addition, central bankers, gathering this week for the Federal Reserve’s annual Jackson Hole conference in Wyoming could disrupt the upwards trend if the financial stimulus package is reduced too quickly. In September, the Fed is to begin reducing $4.5 trillion in holdings building up over the past decade. Eurozone Economic growth in the eurozone outpaced the U.S. in the first and second quarter of the year. Business confidence is at its highest level in a decade, with unemployment falling to an eight-year low of 9.1%. Spain recorded its best growth performance in nearly two years in Q2 2017, with France and Portugal also producing solid growth. In Italy, exports are up 8% from the previous year. Even troubled eurozone economies, such as Greece, are finally show signs of strength. The OECD is predicting 1% growth for Greece this year. This is the best performance projected for the nation in over a decade. In July, Greece returned to the international bond market after being locked out since 2014. Japan Japan’s economy grew 4% in the three months through June, extending its most recent streak of growth under Prime Minister Shinzo Abe. One of the primary drivers of growth is consumer spending; Nissan Motor Co. saw a rise in Japanese sales by 46% in June thanks to the popularity of newly released models. Emerging Markets The rebound of the Commodity market has produced a new sense of confidence in emerging markets. The IMF’s global price index for all commodities is up 27% from the start of 2016. The Brazilian economy is now forecast to expand 0.3% in 2017. While this outlook hinders the U.S. equity market, investors in other countries have benefited: Indexes in Hong Kong, Turkey, Argentina, Poland and Greece are all up more than 20% this year. Conclusion In July, the IMF projected global economic output would increase 3.5% in 2017 and 3.6% in 2018. The growth increase is lifting the spirits of investors and boosting economic confidence throughout the world. For other articles by Keith Knutsson see the following links: Blog here Twitter here Facebook here Instagram here |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

October 2018

CategoriesAll Investing Keith Knutsson Real Estate Real Estate Investing |

RSS Feed

RSS Feed