|

Low inventory and interest rates in the real estate sector colluded to attract foreign investment, surging prices in the housing market of Australia in the past. According to the Bureau of Statistics, Sydney’s residential property price index has increased some 70% during the past five years, reaching a peak in 2014. The real estate industry’s outlook remains strong, even though growth rates are expected to slightly decelerate overall in the coming years due to government intervention on foreign investments.

Especially China, the biggest group of foreign buyers in the Australian real estate market per the Foreign Investment Review Board, has been deterred from further investments. From 2015 to 2016, Chinese investors spent $32 billion, mostly in Sydney and Melbourne, four-times the amount US residents spent. Foreign investment in the past has been restricted to only new developments, but with recent regulations Rules for developers have changed too - now only half the dwellings in new developments can be sold to foreign investors. Additionally, the government has enacted charges of between 1.4-to-5.5 per cent — depending on the value of the property— as well as a vacant property tax of 1 per cent. Keith Knutsson of Integrale Advisors commented, “Regulation on foreign investment certainly slows down asset management services in Australia, but building and construction contractors as well as property agencies will remain, with increasing strength, to be key suppliers to this low inventory market. Australia is continuing to look for those services, no matter where the capital originates from. Yet, enormous capital requirements might limit new entrants from entering the market.”

0 Comments

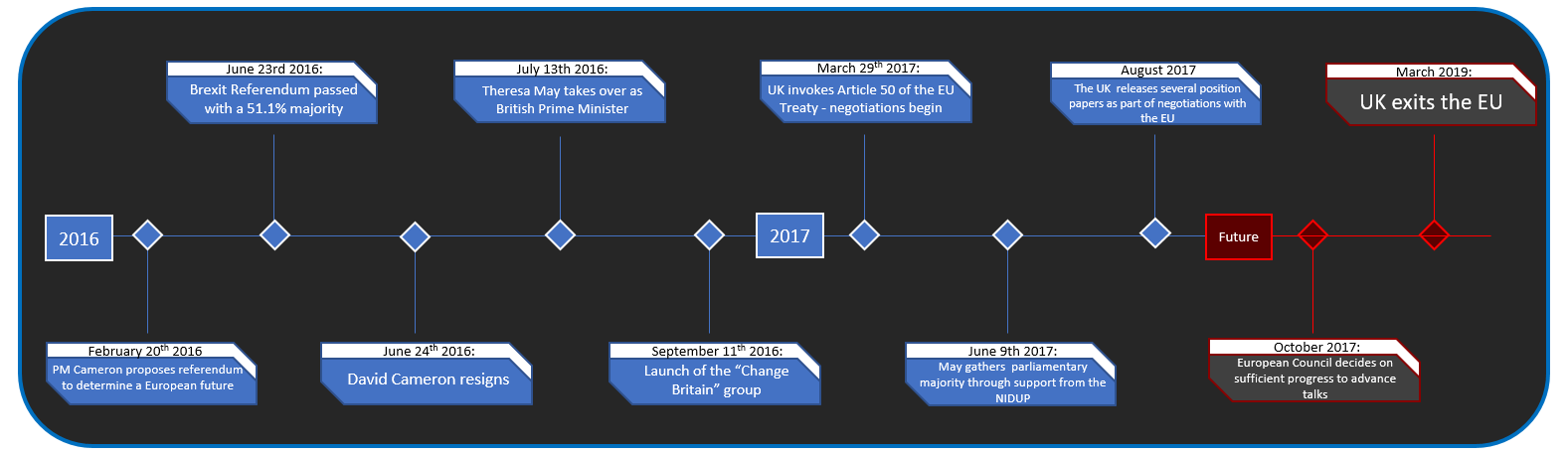

As the clock on Brexit negotiations is ticking, Britain’s political winds are shifting. In two months, the European Council decides whether Brexit negotiations can advance to focus solely on future relationship and any potential transitional deal based on a report of the Chief negotiator Michel Barnier. Currently the logistics of managing the actual political exit of Britain are slowing down proceedings. To understand future developments, it’s vital to begin with an understanding of the events leading up to Brexit. Keith Knuttson of Integrale Advisors says:” Over the past few months an array of invalidated speculation has played a part in shaping the misunderstandings regarding the proceedings in the UK. It is vital to remain conscious of ideas that were based on erroneous information.” David Cameron spoke of Brexit for the first time in February 2013: a referendum on Britain’s membership to the EU if the Conservative party is elected in the next general election. At the time, Cameron was trying to quell euro-skeptics within his own party. A year and a half later Scotland held a referendum on its own independence from the UK, but voters wanted to remain in the UK. The sentiment of Scots to remain in the UK and Europe caused further division within Brexit negotiations months later. In May 2015 Cameron’s party wins and British voters elect a majority Conservative government. During his victory speech Cameron mentions that there will be a referendum on EU membership. Cameron announces that he has negotiated a deal with EU leaders which will give Britain a “special status” if it stays in the EU. Then on February 2016 Cameron announces his official position and starts to campaign for the remain movement. A previous political ally to Cameron, Boris Johnson, proceeds to join the leave campaign on February 21st – shifting tides towards Brexit. On June 16th 2016 ardent remain campaigner Jo Cox is shot and stabbed in the street in her electoral district in northern England by the extremist Thomas Mair who shouted “Britain first, Keep Britain independent, Britain always comes first.” Both sides temporarily suspended campaigning ahead of the referendum. One week later the UK voted 51.1% in favor of Brexit with a turnout of 72.2%.  8/27/2017 0 Comments The Global EconomyThe world’s major economies are growing harmoniously, a result of persistent low-interest-rate stimulus from central banks around the world and the rise out of debt for nations faced with political and economic uncertainty, such as Greece and Brazil.

The OECD, Organization for Economic Cooperation and Development tracks the progress of its 45-member states. These nations are on track to grow this year, and 33 of them are projected to accelerate significantly from the previous year, according to the OECD. “For the first time in years we are seeing signs of continuous, synchronized economic expansion on the international front” said Keith Knutsson of Integrale Advisors. U.S. U.S. exports rose 6% in the first half of the year, the best two-quarter performance since the end of 2013. The post-election period has been categorized by economic strength as well record-breaking index growth, such as the DJA and Nasdaq averages. In addition, central bankers, gathering this week for the Federal Reserve’s annual Jackson Hole conference in Wyoming could disrupt the upwards trend if the financial stimulus package is reduced too quickly. In September, the Fed is to begin reducing $4.5 trillion in holdings building up over the past decade. Eurozone Economic growth in the eurozone outpaced the U.S. in the first and second quarter of the year. Business confidence is at its highest level in a decade, with unemployment falling to an eight-year low of 9.1%. Spain recorded its best growth performance in nearly two years in Q2 2017, with France and Portugal also producing solid growth. In Italy, exports are up 8% from the previous year. Even troubled eurozone economies, such as Greece, are finally show signs of strength. The OECD is predicting 1% growth for Greece this year. This is the best performance projected for the nation in over a decade. In July, Greece returned to the international bond market after being locked out since 2014. Japan Japan’s economy grew 4% in the three months through June, extending its most recent streak of growth under Prime Minister Shinzo Abe. One of the primary drivers of growth is consumer spending; Nissan Motor Co. saw a rise in Japanese sales by 46% in June thanks to the popularity of newly released models. Emerging Markets The rebound of the Commodity market has produced a new sense of confidence in emerging markets. The IMF’s global price index for all commodities is up 27% from the start of 2016. The Brazilian economy is now forecast to expand 0.3% in 2017. While this outlook hinders the U.S. equity market, investors in other countries have benefited: Indexes in Hong Kong, Turkey, Argentina, Poland and Greece are all up more than 20% this year. Conclusion In July, the IMF projected global economic output would increase 3.5% in 2017 and 3.6% in 2018. The growth increase is lifting the spirits of investors and boosting economic confidence throughout the world. For other articles by Keith Knutsson see the following links: Blog here Twitter here Facebook here Instagram here New York City office landlords are increasing their use of “goodies” such as free rent periods and remodeling money to incentivize tenants to rent space, according to market reports.

These benefits are commonly known as concessions, hitting a record $173/sq. ft. in the first quarter in Midtown, up 3.3% from the previous year. This comes as a result of increased competition from new office space, specifically in West Side Manhattan. Not long ago, owners of office buildings were offering rent reductions between five to seven months and tenant-improvement cash contributions of up to $70/sq. ft. Today, tenants get offers of anywhere from 12 to 15 months of free rent and landlord contributions between $85 and $100/sq. ft. While these concessions have been rising since the recession, brokers and analysts remain cautious. For example, historically low interest rates, have made concessions more affordable to landlords than that of previous real estate cycles. “Higher concessions are not a sign of a weak market. As long as interest rates remain relatively low, owners would rather offer concessions today for higher rent profits in the future.” said Keith Knutsson of Integrale Advisors. Landlords interested in boosting rent levels in order to maintain or increase the building’s value can negotiate higher rents with tenants, offering to cover a significant portion of construction costs and sometimes even take on the task of an office buildout, remodeling office space. They can make their returns when they refinance, recapitalize or sell their properties. Amid investors, thoughts remain on the enigmatic question of “how long can this last?” After eight years of economic expansion, investors are starting to wonder when the real estate contraction will happen. Ryan Severino, chief economist for JLL in New York, believes “we have at least a couple of years before we start to have that question about is the clock ticking or not.” Some would argue this is a rather optimistic opinion and align their sights more so with the ‘Skyscraper Effect,’ which is an economic indicator suggesting recession follows the construction of the world’s tallest buildings.

There is no arguing that we are late in the cycle, but depending on the market sector and asset type, additional investigation is required. Softening areas include central business districts (CBD), high street retail, and CBD multifamily. However, strength continues in suburban multifamily, class B and C multifamily, suburban office, and industrial sectors. It is also important to note that market cycles vary greatly based on geography as “[t]here is no such thing as a national real estate market. Every market and economy is local in nature,” adds Ted C. Jones, Ph.D., chief economist and senior vice president at Stewart Title Guarnty Co. in Houston. Jones along with others, forecast a bullish overall outlook on the economy. Keith Knutsson of Integrale Advisors, states “there is still upside potential for the remainder of this fiscal year, however, market shifts will present themselves in the near future.” Employment rates will remain high, but there will be lower levels of growth according to the Urban Land Institute (ULI). New Trump fiscal stimulus policies remain in question, particularly with the tax reform, which will greatly affect the amount of growth. 7/21/2017 0 Comments IMF Board is set to Bailout GreeceThe International Monetary Fund’s recent activities have led to the approval of the latest Greek bailout. The news keeps pressure on Europe to further deliver debt relief and will prevent Greece from raising capital in markets for the time being. Greece’s IMF bailout sets a debt ceiling for the central government around €325 billion, accounting for the country’s current debt and the bailout funds it receives from its European creditors. “The IMF board has approved Greece’s bailout, in part as a reaction to current levels of debt, unemployment, and GDP which have been deemed unsustainable by the global community” said Keith Knutsson of Integrale Advisors. According to an earlier version of the document prepared in April, the ceiling of €325 billion was initially imposed on the general government debt, giving Greece a buffer of around €10 billion. The following provisions will force Greece to focus on implementing reforms agreed under the bailout such as amending the pension system and privatizing public industries. The European Central Bank, International Monetary Fund, the administration of Athens have not been to reach a viable solution for years. However, the beginning of the country’s third bailout program should provide the necessary relief for Greece moving forward. The involved parties reached a compromise last month when the Europeans agreed to a limited aspect of debt relief that will be implemented after the bailout ends. The IMF agreed to support a new program “in principle,” but would only distribute financing once Greece takes the necessary steps to fixing the structural issues in their economy. Despite the lack of a clear and feasible solution, the result of recent bailout negotiations created a sense of positive momentum for the Greek economy. The country’s borrowing costs have dropped, Moody’s rating agency upgraded the economic outlook, and the European Commission suggested that the EU should no longer enforce disciplinary measures. Despite the challenges faced, the Greek government is planning to enter the bond markets in the coming days with an issuance that will be mainly covered through swaps of a bond program that expires in 2019.2016 was a standout year for real estate performance in Ireland. According to the Financial Times, Ireland was the “fastest-growing economy in the EU.” CBRE’s Europe Real Estate Market Outlook 2017 forecasted this trend will continue into 2017 and 2018. The research cited rental incomes increasing 11% year on year (Q3 2015 – Q3 2016) largely due to high demand outweighing the low supply in the housing market. However, the Irish government addressed the supply concern by initiating a number of development projects. Many of these projects are now transitioning from conceptual or early planning phases to the beginning of site work. Fortunately, multi-family investors should expect rental inflations to continue through the remainder of 2017 and into the coming years.

|

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

October 2018

CategoriesAll Investing Keith Knutsson Real Estate Real Estate Investing |

RSS Feed

RSS Feed